Introduction

Money is more than just a few digits in an account; money represents status, freedom, security, or even love. When we purchase something, we don’t typically make the decision by simply weighing the facts; we are driven by powerful psychological influences. By understanding the psychology of money, you will become a better financial decision maker, less stressed out, and ultimately, build wealth.

How Our Minds Drive Financial Decision Making

Humans are first emotional and second rational. Behavioral economists examine how people behave when dealing with money and have found that our money choices are illogical and are made subconsciously based on feelings, habits, and social cues.

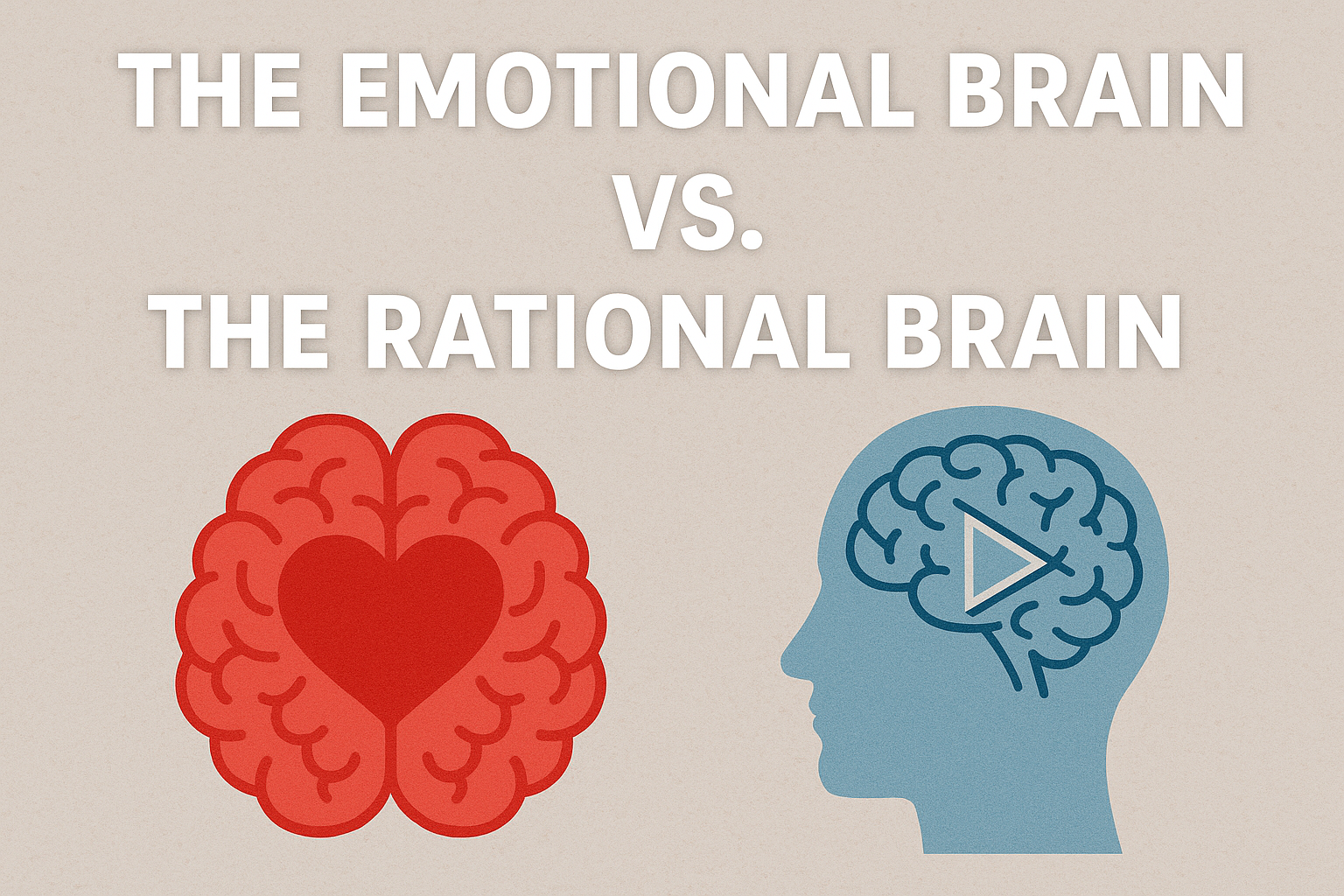

The Emotional Brain vs. the Rational Brain

When we make a buying decision, two parts of the brain are uniquely engaged in a subtle battle:

- The limbic system gives rise to desire and reward.

- The prefrontal cortex makes rational thoughts and long-range plans.

Once the emotional brain wins, we buy the expensive shoes or the shiny new phone, regardless of our budget or larger life plan.

Common Cognitions Biases that Affect Spending

We experience several common cognitive biases, or mental shortcuts, that shape how we spend our money:

Loss Aversion

When it comes to money, we fear losing it more than we care about actually gaining it. You can see why sales with “limited time only” work so well to trigger a sense of urgency.

Present Bias

We also fail to save, because we prioritize real-time gratification over saving for the future. After all, it is easier to justify having dinner out as opposed to making a contribution to your retirement.

Anchoring

When we see a price for the first time we create an “anchor” in our mind. After seeing a $500 jacket, a $150 jacket looks “cheap”.

Cultural and Social Influences on Money

The way we view money is shaped by nuanced influences from upbringing, culture, and peer group.

Family Money Scripts

If you had a childhood where money was scarce, you may spend irrationally in an attempt to feel secure. Or, if you come from a wealthy family, you may view spending as a signal of freedom.

The power of social proof

We want to fit in with other people. When we see friends in luxury vehicles, or wearing designer clothing, we feel social pressure to match their lifestyle, even if it comes with financial strain.

Media and Marketing

It is important to remember that advertisements and brand marketing target our deepest emotions such as love, success, belonging, and self-esteem. Brands don’t just sell things; they sell identity.

Emotional Triggers to Spend More Money

Certain emotions can open the wallet quicker than any type of logic can intervene.

Retail Therapy

Shopping provides a dopamine hit that can temporarily alleviate boredom or sadness—but this high wears off quickly often resulting in remorse and credit-card debt.

FOMO

In today’s environment, limited-time offers and social media trends make being stuck in your own frame of mind often feel like missing out, as if you are losing or being left behind just by waiting.

Celebration and Reward

A large portion of the population has a celebration habit, often making larger purchases to mark the occasion. A new car after a promotion, or a nice vacation after a stressful year.

Practical ways to get control back over your money psychology

Awareness is very powerful, but you need to take action to secure your financial future. Here are some evidence-based practices to help you get back control:

Build a Conscious Spending Plan

Limit deprivation, instead, plan for your money:

Needs: rent, food, utilities

Wants: entertainment, travel

Savings: emergency fund, retirement

You can use this framework to satisfy emotional urges without compromising your financial health.

Wait 24 hours before all unplanned purchases

Give yourself a good night’s sleep before plunging into that unplanned purchase. Wait one full day, most “must-have” items will lose their attractiveness by waiting until the next day.

Automate Good Habits

Set up automatic transfers to savings or investment accounts! At that point you are taking willpower out of the equation.

If you can, track your emotional spending

Keep a journal for a month about how you are feeling, and how you feel after you purchase something. You will start to see patterns.

Summary

Most money decisions are emotional. Acknowledging cognitive biases is the first step to taking control.

Culture and peers shape spending habits. Awareness of these influences allows breaking unhealthy emotional cycles.

Things you can do such as automation and the 24-hour rule create distance between impulse and action.

Investing takes patience and emotional equilibrium. Don’t let fear influence decisions.